Life Insurance in the Age of COVID

One aspect of the current pandemic that nobody seems to be talking about is the impact of those hundreds of thousands of COVID deaths on the life insurance industry—and on policyholders. A recent panel discussion using actuarial data estimated that if the current pandemic were to reach death rates equal to 1918—clearly a worst-case scenario now that vaccines are widely available—the increased insurance payouts would total $117 billion. A lower estimate, which is more in line with the existing coronavirus morbidity, would put that figure at $20 billion. In either case, the government-mandated reserves (money basically held in escrow to pay out to policyholders) of 70% of the total death benefit face amounts is more than sufficient to cover even the higher of these additional costs.

Another impact, which can be overlooked in this equation, is that life insurance sales have declined during the pandemic year, in part due to the slowdown throughout the economy, in part due to the fact that life agents were forced to sell remotely rather than face-to-face. But, at the same time, fewer people with existing life insurance are cancelling their contracts or declining to pay premiums—almost certainly because the risk of dying has increased.

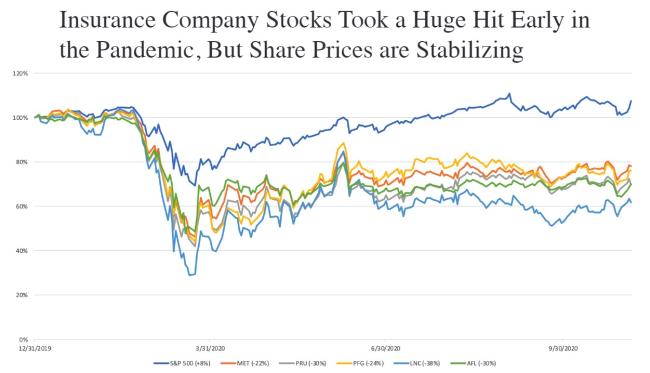

The full impact on the life insurance industry won’t be known for another few months, but you can get a sense of it by looking at the decline in stock prices of the major life insurance companies (see chart). The blue line at the top is the S&P 500 index, which took a big hit in March of 2020 and has largely recovered since. The insurance companies, which were expected to be among the biggest losers as people realized the scope and severity of the pandemic, saw their stock values decline even more, but have since recovered—albeit at a lower level.

The first thing that people who currently have a life policy should know is that their policies will cover them if they pass away due to COVID-19. Life insurance companies are not allowed to change the terms of coverage for active policies. A more interesting question is whether rates will become more expensive in the future. It is probable that people who have survived a coronavirus infection will have to disclose this on their policy application, and will have to pay higher rates, due to the possibility of prolonged health effects.

A number of insurance companies are following the lead of other industries and offering grace periods on premiums for people who have suffered economic hardship as a result of the pandemic. People who have group coverage through their employer with MetLife, for example, can continue to receive coverage for 12 months after they are furloughed or laid off, provided they keep paying the premiums. Northwestern Mutual allows customers to suspend their premium payments for 90 days due to economic hardship and still remain covered, while MassMutual has gone so far as to offer free three-year term policies to people in some of the riskiest corners of the economy: frontline workers such as in-hospital personnel and first responders.

sources:

https://www.valuepenguin.com/life-insurance-coronavirus-faq

https://www.actuary.org/sites/default/files/2020-11/COVID-19-Combined.pdf