Discover Effective Planning and Investing Strategies for Higher Education

Discover effective planning and investing strategies for higher education

Investing for college can be daunting. Listed here are some investment choices designed to help take you where you want to go.

Understanding the basics

Setting aside funds for higher education can create a brighter future for you or a loved one, but deciding how to go about investing can leave you guessing. If you are setting aside funds specifically for education - then vehicles like a 529 College Savings Plan and Coverdell Education Savings accounts offer tax-deferred or even tax-free growth so you can maximize your potential savings. Whichever approach you select, it's important to remember that starting early and contributing even just a little bit regularly can help you reach your goals faster.

Investment Vehicles Designed for Education

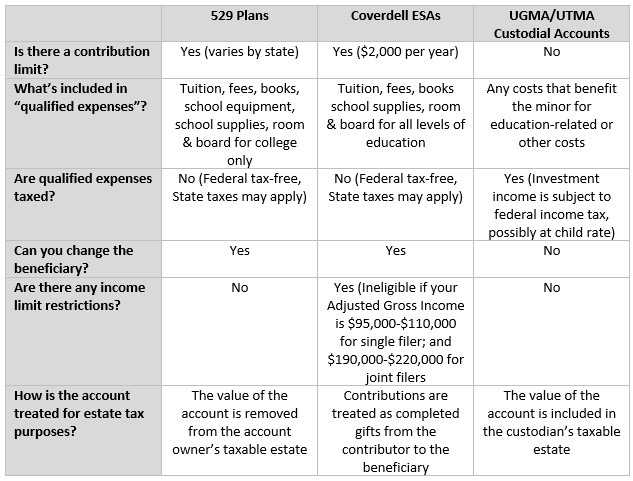

There are a number of choices available for those seeking tax-efficient accounts specific to education. These include the 529 College Savings Plan, Coverdell Education Savings accounts, and UGMA/UTMA Custodial accounts.

529 Plans

Sponsored by individual states, these college savings plans offer a level of flexibility and potential tax advantages that can make them a great choice for the right investor. Benefits of a 529 plan vary from state to state. Details of a 529 College Savings Plan include:

-

The account owner maintains control over the account even if the beneficiary decides not to go to college

-

Allocate assets based on risk tolerance or child's age

-

Contribute $400,000 in a liftetime per beneficiary1

-

Contributions and earnings grow federal tax-deferred and funds withdrawn for qualified higher education expenses are completely free from federal income taxes

-

Some states may offer tax benefits to in-state residents2

-

Invest as much as $15,000 per year per child, or $75,000 in a single year, without incurring federal gift taxes3

Coverdell Education Savings Accounts

These accounts offer federal tax-free earnings and withdrawals on qualified expenses such as tuition, books, computers, and room & board. While 529 Plans are used exclusively for college. Coverdell Education Savings Accounts (ESAs) can be used for elementary and secondary schooling, in addition to college. Additionally, there are no minimum contributions, and account owners can contribute up to $2,000 per child per year.

UGMA/UTMA Custodial Accounts

Custodial accounts provide a way to build assets for your children or loved ones future and let you manage a minor's assets for their benefit. As you build a portfolio, with or without assets from the minor, you will be the guardian of the account, managing it until the minor reaches the age of majority. From the start, the account will be held under the minor's name and Social Security Number. Once they are old enough, they will assume control of all assets.

Compare Education Investment Vehicles